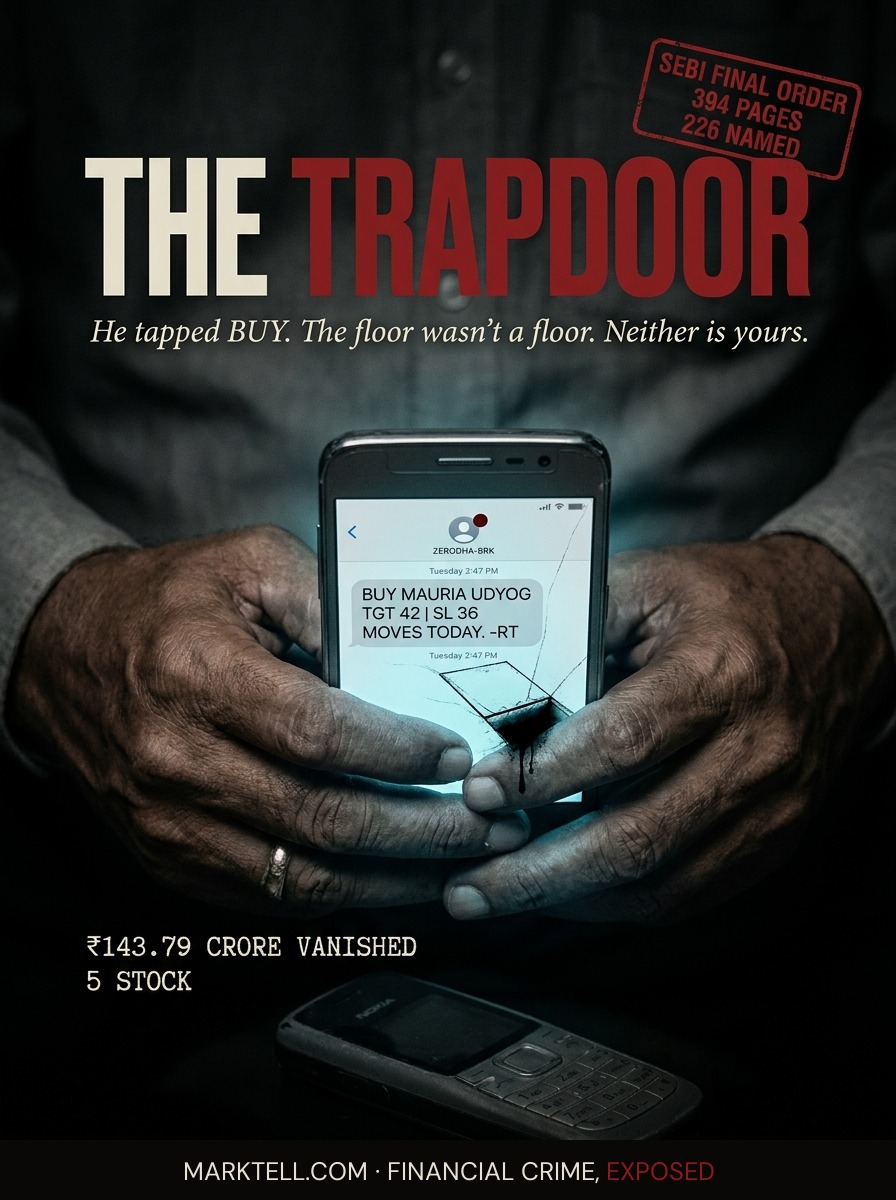

The SMS said Zerodha. The SMS was the trapdoor.

A ₹143.79 crore ($17M USD) stock manipulation ring in India ran on text messages that looked like they came from Zerodha and ICICI. SEBI's 394-page final order names Hanif Shekh at the center and penalizes 225 others around him.

Rakesh kept two phones on the desk in the second bedroom. The Nokia was for his wife, his sister in Pune, and the parents of the students he taught at the government school in Nagpur. The Android was for the market. He was fifty-four. He had been buying shares in small lots since 2011, mostly on tips from a cousin who worked at a bank, and after the cousin retired, mostly on tips that arrived by SMS.

On a Tuesday afternoon in 2019, the Android buzzed. The sender ID on the screen read like the name of a broking company he recognized. Not exactly. Close enough. The message told him a stock called Mauria Udyog was about to hit a target. It gave him a buy range. It gave him a stop loss. It ended with the kind of two-letter sign-off that broker research desks use.

He did not check the sender ID against the actual sender ID of the broker whose app was already open on the same phone. Nobody does. The message looked like the last twenty messages that had looked like it.

He bought.

I.

SEBI released a 394-page final order this week. That is the document at the center of this story. It names Hanif Shekh as the person who ran what the regulator describes as a coordinated pump-and-dump operation across five listed companies between 2017 and 2020. Mauria Udyog Ltd. Vishal Fabrics Ltd. 7NR Retail Ltd. GBL Industries Ltd. Darjeeling Ropeway Company Ltd.

A pump-and-dump is a structure, not a mood. It has parts. First, the operators accumulate a position in a stock that does not trade much. Low liquidity is a feature, not a bug. It means a small amount of buying can move the price a large amount. Second, the operators create the appearance of demand. They trade shares between accounts they control to make the volume look real. This is called wash trading. Third, they send messages to retail investors telling them the stock is about to move. Fourth, the retail investors buy. The price rises. Fifth, the operators sell into that buying. Sixth, the messages stop. Seventh, the price falls back to what the stock was worth before the operators arrived, which is not much.

SEBI's order puts the unlawful gains from this specific scheme at ₹143.79 crore (about $17M USD). It penalizes Shekh ₹10 crore ($1.2M USD) and bars him from the securities market for seven years. It penalizes 225 other individuals and entities in a ring around him. Five entities SEBI identifies as Shekh-controlled, including Robert Resources Ltd, Econo Trade India Ltd, Econo Broking Pvt Ltd, and Sai Metaltech LLP, were each fined ₹2 crore ($240K USD) and restrained for six years. Most of the others were fined ₹5 lakh ($6K USD). Twenty-three received ₹50 lakh ($60K USD) fines.

Two hundred and twenty-six names on a single order. Read that slowly. A pump-and-dump at this scale is not a person with a phone. It is a staffing chart.

II.

The trapdoor is the SMS.

That is the image to hold. Not a boiler room. Not a Zoom call. A text message that arrives on a Tuesday, from a sender ID that has been engineered to look like the name of a real brokerage. SEBI's findings describe fake sender IDs designed to resemble prominent equity broking companies. The names in the record include Zerodha and ICICI Securities. Rakesh did not know these were fake. Neither did the thousands of other retail investors whose buying moved the price at the exact moment the ring wanted it moved.

The floor of the trapdoor is the recommendation. The hinge is the sender ID. The room below is the ring's sell orders, already resting on the book, waiting.

Rakesh's Android buzzed. He read the message. He tapped buy. He watched the price move up over the next two sessions, exactly as the message had said it would. He felt what people feel when a tip works. Not greed. Something closer to relief. The relief of being on the right side of a thing for once.

Then the price stopped moving. Then it fell. He held. He was told to hold, by another message from the same sender, promising the correction was temporary. The correction was not temporary.

III.

What was on the other side of the trapdoor.

SEBI's order describes the ring's architecture in categories the regulator has been refining for years. There were price-volume influencers, whose job was to create artificial trading momentum by moving shares between accounts on cue. There were promoter-linked off-loaders, whose job was to hold the shares that would be sold when the retail buying arrived. There were financing entities, whose job was to move money into the trading accounts before the accumulation and out of them after the sale. There were conduit companies, whose job was to make the money's path hard to follow.

Two hundred and twenty-five entities. That is the size of the crew. That is what it takes to run a pump-and-dump across five stocks over three years without the pattern showing up on the exchange's surveillance screens for a long time.

It did show up eventually. SEBI notes that the manipulated stocks had low liquidity and no significant corporate developments during the period the prices surged. In the language of the market, nothing was happening at the companies. Only in the tape.

Not turbulence. A pattern.

IV.

Rakesh does not know these terms. He does not need to. He knows that the tuition fund he had built for his son's engineering coaching lost more than half its value between the buys he made on those SMS tips. He knows he did not tell his wife the whole number. He told her the market had been volatile. He used the word volatile because it is the word that has been given to men like him to describe what happened to their money, when the word that fits is not volatile.

He still keeps the two phones on the desk. The Nokia is for family. The Android is for the market, though he has stopped acting on tips. He reads the messages when they arrive. He looks at the sender IDs now. Some of them still look like the names of brokers he recognizes. He is not sure whether the ones that arrive now are real or fake. Neither, if we are honest, are you.

V.

Hanif Shekh has been on SEBI's radar for years. The regulator fined him ₹7 lakh (about $8K USD) in November 2022 for evading summons. Reporting from 2023 places him outside India, reportedly in Dubai. His own social media at that time described him as an entrepreneur, a private equity investor, a green-ship recycler, and the managing director of Econo Broking. Earlier reporting referenced a broader ₹1,500 crore ($180M USD) SMS stock tip scam attributed to him. This week's order is narrower. It quantifies the unlawful gains from the five specified stocks at ₹143.79 crore ($17M USD) and attaches names, penalties, and market bans to the ring around him.

An order is not a recovery. A penalty is not a refund. The seven-year ban runs from the date of the order forward. The stocks Rakesh bought are still listed. The messages that told him to buy them arrived seven years ago and were deleted a long time ago from a phone he has since replaced.

The regulator has done what a regulator can do. It has named the machine. It has counted the parts. It has published the 394 pages.

The machine is a text message that looks like it came from your broker. The trapdoor is the sender ID. Rakesh stepped on a floor that was not a floor. So did enough people to move the price of five stocks by ₹143.79 crore ($17M USD).

He did not tell his wife the whole number. He is still not going to.

- Moneylife | July 1, 2026 | "Stock Manipulation: SEBI Slaps ₹10 Crore Penalty on Hanif Shekh, Penalises 225 Others in ₹143.79 Crore Scheme"

- SEBI | 2026 | 394-page final order in the matter of Hanif Shekh and connected entities

- SEBI | November 2022 | ₹7 lakh penalty on Hanif Shekh for evading summons

- SEBI | May 2026 | Order barring seven entities in social media SME manipulation network, ₹20.25 crore impounded

- SEBI | June-July 2026 | Order barring 10 individuals in Darjeeling Industries Ltd manipulation case

- Prior reporting (2023) | Reports on broader alleged ₹1,500 crore SMS stock tip scheme attributed to Shekh

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.