The collateral was real. Until it wasn't. Then it was paper.

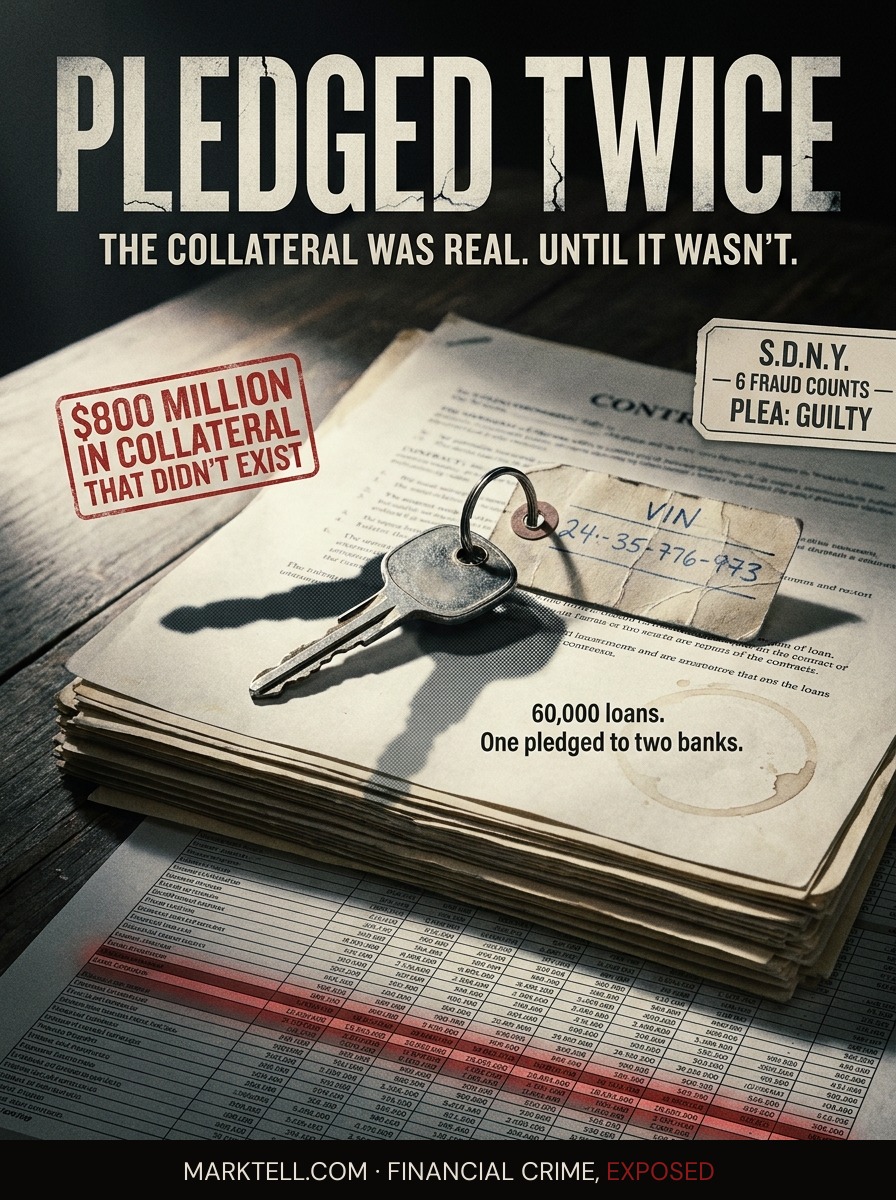

On June 24, 2026, Tricolor's former COO admitted he helped pledge the same car loans to multiple banks. The borrowers were Hispanic immigrants buying used cars. The shortfall was eight hundred million dollars.

Marisol signed the loan in a dealership off Harry Hines Boulevard in Dallas in the spring of 2023. The car was a 2016 Nissan Altima, silver, one hundred and twelve thousand miles on it. The salesman spoke Spanish. The paperwork was in Spanish. The monthly payment was four hundred and seventy-three dollars and it was, she thought, the closest thing to a fair deal she had been offered since she came to Texas.

She needed the car because her son had dialysis three days a week, and the bus did not run on the schedule his blood needed.

She remembers the key. It came on a little paper tag with the VIN written on it in blue pen. She remembers the coupon book that arrived in the mail two weeks later, a small stapled rectangle of due dates. She put it in the drawer next to the dialysis appointment card and the electricity bill. That drawer was the budget.

She was not a mark in the way the word usually works. She got a car. The car ran. She paid every month and the payments cleared. From her kitchen table in Oak Cliff, the loan was the loan.

She did not know her loan had been promised to two different banks.

I.

Tricolor Holdings called itself a Community Development Financial Institution. The federal government had certified it as one. The pitch, in the company's own materials and in the lenders' marketing decks, was that Tricolor was building credit for working Hispanic families who had been frozen out of mainstream auto finance. Buy here. Pay here. Build a file. Drive to work.

At its peak, the company had a five-billion-dollar loan portfolio and more than sixty thousand car loans on its books, according to bankruptcy filings.

On June 24, 2026, the former Chief Operating Officer of that company, David Goodgame, 49, pleaded guilty in the Southern District of New York to six fraud and conspiracy counts. Bank fraud. Securities fraud. Wire fraud. Conspiracy. False statements. The most serious of those carries a maximum of thirty years.

He admitted, according to the plea, that he knew Tricolor was deceiving the banks. He admitted he knew the data was being manipulated.

That is what the loan tape was. A spreadsheet. Tens of thousands of rows. Each row a borrower, a car, a payment history, a loan-to-value ratio, a delinquency status. The banks lent against that tape. The banks audited that tape. The banks designed eligibility rules around that tape.

Prosecutors allege the tape was, in places, a costume.

II.

There is a phrase in the indictment that does the work of a hundred others. Double-pledging.

It means this. You take a loan, a real loan, like Marisol's, and you pledge it as collateral to Bank A in exchange for a line of credit. Bank A advances you money against it. Then you take that same loan, that same VIN, that same borrower, and you pledge it again to Bank B. Bank B advances you more money against it.

The car exists. The borrower exists. The payments exist. But the collateral has been sold twice.

The federal complaint against the company's executives alleges that by August 2025, Tricolor had pledged approximately $2.2 billion in collateral to its lenders and investors. The real collateral, the loans that had not already been promised to someone else, totaled about $1.4 billion.

The difference is eight hundred million dollars.

Read that slowly. Eight hundred million dollars of collateral that, when the banks went looking for it, was not there. It had been counted. It had been listed. It had been signed for. It had not existed in the form the lenders thought they had bought.

The second technique, the one Goodgame admitted to helping run, was uglier in its small ways. Prosecutors allege the company manipulated the characteristics of individual loans on the tape. A loan that was too delinquent to qualify for a particular facility was groomed on paper until it qualified. A car whose value had cratered was assigned a value that let the loan stay inside the box. A near-worthless asset was dressed in language the eligibility rules would accept.

Marisol's loan was probably not the one they were rewriting. Marisol's loan worked. That is the thing about this kind of fraud. It needs the real loans. The real loans are what make the fake loans plausible.

She was, in the language of the machine, fuel.

III.

JPMorgan Chase took a $170 million charge-off on its Tricolor exposure, according to its public disclosures. Fifth Third Bancorp recorded an impairment charge of between $170 million and $200 million. Barclays, according to reporting, faces hundreds of millions in losses.

Those are big banks. They have credit committees. They have collateral auditors. They have entire departments whose job is to verify what they are lending against.

On June 10, 2026, a federal judge dismissed a civil suit brought by investors who had argued that JPMorgan, Barclays, and Fifth Third had ignored what the complaint called giant red flags while marketing Tricolor's debt to others. The court did not find the banks innocent of inattention. It found the plaintiffs had not stated a claim that survived the motion to dismiss. Those are different things.

What the civil docket cannot do, the criminal docket may. Goodgame has agreed to cooperate with the government. Former CFO Jerome Kollar and former finance executive Ameryn Seibold pleaded guilty in December 2025 and are also cooperating. Former CEO Daniel Chu, indicted on an expanded eight-count indictment on June 24, 2026, has pleaded not guilty. His lawyer says he intends to fight the charges at trial. The trial is scheduled to begin on October 19, 2026.

Allegation is not adjudication. We will say that here because it is true and because Chu has a trial date.

But three of the executives who sat around the table where the tape was built have now said, under oath, that the tape was not what it looked like.

IV.

In August 2025, with the lenders beginning to ask the questions the loan tape could no longer answer, Daniel Chu allegedly extracted $6.25 million in bonus payments from the company, according to the indictment. Prosecutors say a portion of the money was used to buy a multimillion-dollar property.

Picture the timing. The banks are inside the books. The collateral discrepancies are surfacing. The credit lines that fund the next month's payroll are about to close. And the wire goes out. Six and a quarter million dollars. To the founder.

On September 10, 2025, Tricolor filed for Chapter 7 bankruptcy. Not Chapter 11. Chapter 11 is the kind of bankruptcy where a company tries to reorganize, to keep operating, to come out the other side. Chapter 7 is liquidation. The lights go off. The assets are sold. There is no other side.

More than a thousand Tricolor employees were placed on unpaid leave. The dealerships closed. The phone lines went to voicemail.

And the sixty thousand loans on the books, including Marisol's, dropped into the estate.

V.

Marisol kept paying.

She did not know the company was gone for almost two weeks. She found out from a coworker whose nephew worked at a dealership in Garland. She called the number on the coupon book. The number was disconnected. She called the other number she had, the one in the welcome packet. It rang. Nobody answered.

She tried to make her October payment online and the portal would not load.

This is the part the indictment does not contain. The Chapter 7 estate does not file a feeling. But picture her, at the kitchen table, the coupon book in front of her, the dialysis card in the drawer behind it, looking at a screen that will not load and trying to figure out who, exactly, she owes money to now, and what happens to the car if she gets it wrong.

The car was the job. The job was the dialysis. The dialysis was the kid.

That is the chain the loan tape was sitting on top of.

When prosecutors say fraud became an integral component of Tricolor's business strategy, what they mean, translated into the language of the kitchen table, is that the company that sold her the car and held her loan and put her name in a database it pledged to two different banks at the same time was not, in the part of itself that mattered, a lender. It was a machine for converting working borrowers into bank credit, and when the credit ran out, the machine went into the ground and took the borrowers' files with it.

The CDFI badge said community development. The community was the collateral. And the collateral, in the end, was pledged twice.

VI.

Goodgame's plea is one piece. Kollar's and Seibold's pleas are two more. Chu's trial in October is the next one. The civil questions, the ones about what the lenders knew and when, are now on appeal or closed. The industry questions, the ones about how subprime auto securitization handles a corrupted loan tape, are being asked in conference rooms in New York and Charlotte this month.

Marisol is not in any of those rooms.

She is at the kitchen table, with the coupon book, trying to figure out where to send the November payment.

The double-pledge was elegant on paper. One loan. Two creditors. A bridge of fictional eligibility built between them. It worked for years. It paid bonuses. It funded a five-billion-dollar portfolio. It collapsed in a season.

The loans were real. The borrowers were real. The cars were real. The collateral was real.

The only thing that was not real was the idea that it had only been sold once.

- Reuters | June 24, 2026 | "Former Tricolor COO pleads guilty to fraud linked to bankrupt auto lender's collapse"

- U.S. Attorney's Office, Southern District of New York | June 24, 2026 | Plea agreement, United States v. David Goodgame; expanded indictment, United States v. Daniel Chu

- U.S. Bankruptcy Court | September 10, 2025 | Tricolor Holdings LLC, Chapter 7 petition

- U.S. Attorney's Office, SDNY | December 16, 2025 | Guilty pleas of Jerome Kollar and Ameryn Seibold

- JPMorgan Chase & Co. | Q3 2025 disclosures | $170M charge-off related to Tricolor exposure

- Fifth Third Bancorp | Q3 2025 disclosures | $170M–$200M impairment charge

- U.S. District Court, SDNY | June 10, 2026 | Dismissal of investor civil action against JPMorgan, Barclays, Fifth Third

- FBI and FDIC-OIG | June 2026 | Joint investigative materials referenced in DOJ release

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.